Simplifying Complexity: Building an Efficient Cross-Border Payment Experience at Airwallex

Duration

16 Months

Role

UI Designer

Responsibility

User Research, Interaction Design, Visual Design

Company

Airwallex

Project Panorama

01 | Team Goal

To build intuitive, compliant financial infrastructure that transforms complex cross-border payment logic into universal digital efficiency tools for global enterprises and SMBs.

02 | Role & Output

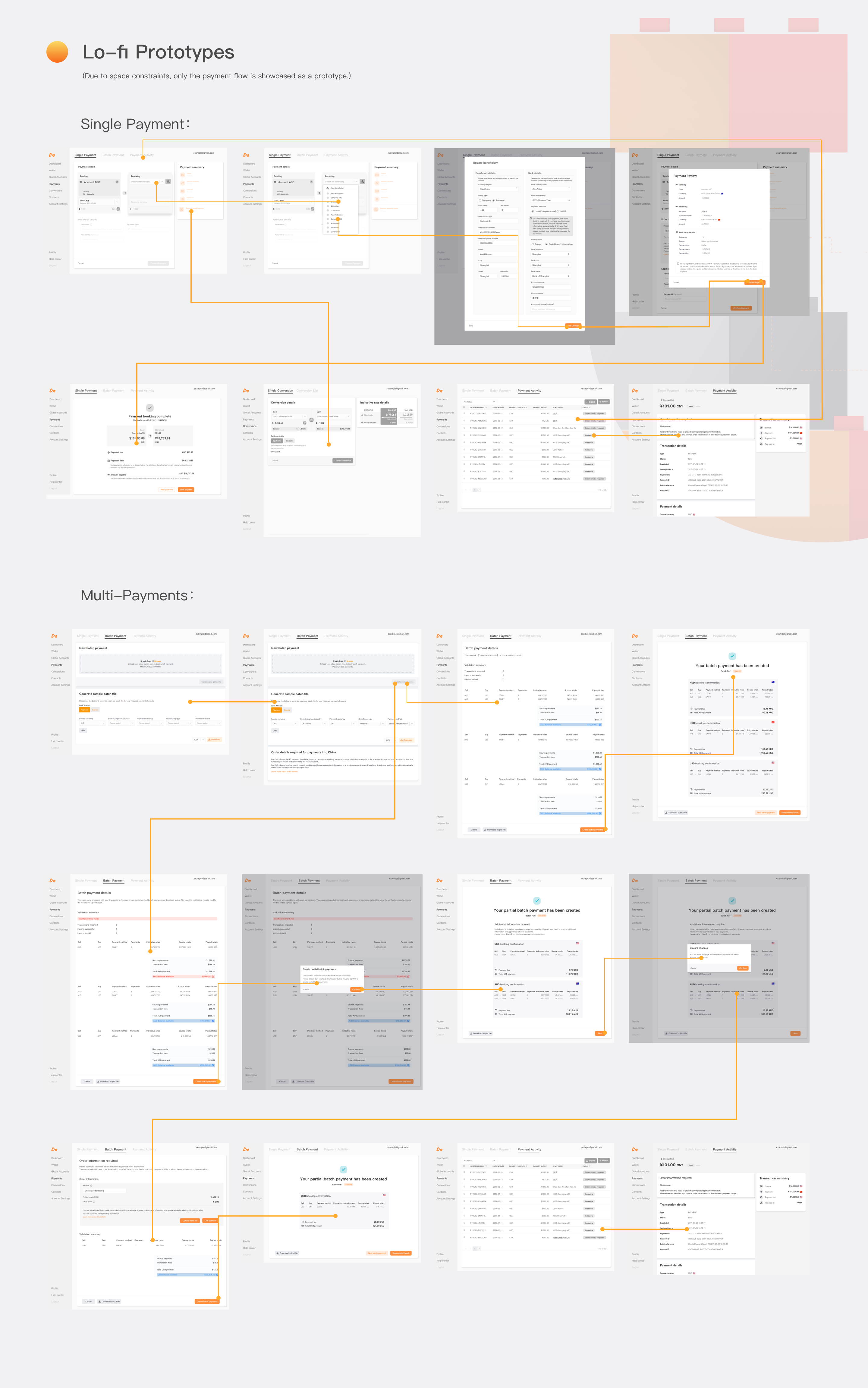

As UI designer, participated in the experience and visual design of payment and FX flows, delivering end-to-end solutions covering complex exchange rate dynamics, fund status tracking, and global compliance validation.

03 | Challenge

Finding the optimal balance between security/compliance and ultra-fast transaction experience amid the diversity of multi-country regulatory policies and real-time second-by-second exchange rate fluctuations.

04 | Impact & Results

Optimized the visual experience of cross-border fund flows, significantly reducing users' FX settlement costs and operational error rates, helping the brand establish professional credibility in the global B2B payment market.

The "2019 SME Cross-Border Trade Research Report" shows that global SMEs account for approximately 78% of total exporters, attracting many innovative payment companies to enter the B2B cross-border payment space. Among them, fintech company Airwallex stands out with its global, integrated cross-border payment platform.

Airwallex's core direction is building a global cross-border payment integrated platform, covering key business areas including cross-border payment and multi-currency FX exchange. Addressing common pain points such as exchange rate volatility, payment security, cost control, and channel limitations, Airwallex flexibly configures product combinations based on specific client needs to provide tailored solutions.

Airwallex Platform Overview

Product Positioning:Through the Airwallex client, users can conduct real-time transactions globally、 account management、 currency exchange and other cross-border transactions

Target Users: Enterprises and cross-border transactions needs, including SMBs

Value: Helping users achieve real-time cross-border transactions, greatly reducing financial and time costs

Design Goals

In discussions with the product manager, we confirmed the overall design goals: by [optimizing client business workflows] and [professional yet intuitive interactions], making transaction flows transparent and clear, improving user satisfaction, thereby providing the foundation for user retention and engagement. Based on this direction, we focused design goals on improving users' understanding and operational efficiency of cross-border payment flows, enhancing trust and satisfaction, and through professional yet easy-to-use interface design, reducing cognitive load and operational error rates.

Target User Groups

After completing design research, we developed diverse user personas, summarizing the main user groups needing cross-border payments: from platform sellers handling high-frequency reconciliation to DTC brands optimizing checkout conversion rates. The design ensures the product precisely addresses unique financial pain points throughout the entire cross-border ecosystem.

Platform Sellers

DTC Brands

Overseas Service Providers & Distributors

Digital-Native Micro Startups

Industry Analysis

In traditional cross-border payment models, common problems are very apparent: unclear fund flows, multiple bank intermediaries, non-transparent exchange rates and fees, unstable arrival times, and low automation efficiency. These issues lead to poor payment timeliness, while customers must also bear potential foreign exchange risks.

Therefore, based on these industry pain points, we need to propose targeted design solutions. Real-time exchange rate quotes, payment node transparency, and user notifications are all areas we can improve at the design level.

Target User Characteristics

Explosive Growth

Rapid growth in China's foreign trade has spawned a large number of cross-border e-commerce platforms

Globality

Built on network development, with global and decentralized characteristics

Intangibility

Digital product and service transmission is prevalent

Immediacy

Information transmission on the internet is near-simultaneous

Paperless

E-commerce trade enables paperless transactions

Rapid Evolution

Rapid development with continuous technological innovation

Cross-Border Payment Enterprise Characteristics

After industry research, I gained understanding of the business logic of cross-border payment companies. I recognized that for a mature cross-border payment service provider, its business usually forms a complete capital flow closed loop. Based on my research, I summarize the business capabilities a cross-border payment enterprise needs as follows:

01 Global Acquiring & Collections

Multi-currency Collections: Support opening virtual accounts for sellers to receive funds from Amazon, Shopify, and other platforms

Acquiring Business: Provide gateway services supporting overseas consumers to pay via international credit cards or local wallets

02 FX Management

Real-time Exchange: Provide real-time exchange services close to mid-market rates

Rate Lock: Help enterprises avoid exchange rate fluctuation risks through technical means

03 Fund Distribution & Payments

International Wire: Support large transfers via SWIFT or local clearing networks

Employee & Supplier Payments: Support global payroll and supply chain settlement, typically with batch payment capability

04 Corporate Card Business

Virtual & Physical Cards: Enterprises can instantly generate virtual cards for paying Facebook/Google ads or cloud service subscriptions

05 Value-Added Services

Financial & Tax Reconciliation: Automatically export transaction statements, seamlessly integrate with various financial software for tax reconciliation

Competitive Analysis

In the highly competitive cross-border payment space, design is not just about aesthetics—it's a game of 'trust' and 'efficiency'. To better understand and position Airwallex in the commercial landscape, I went beyond pure visual comparison and deeply analyzed the underlying business logic of core competitors including Stripe, Wise, and some domestic cross-border payment companies.

In the competitive analysis, I used strategy and functionality as benchmarking dimensions, applying the feature matrix method. By deconstructing these companies' businesses, I tried to find the experience entry point that allows users to feel 'smoothness' even in cumbersome cross-border compliance processes.

Core Business Capabilities

Airwallex (Kuangwai)

Wise (formerly TransferWise)

Revolut Business

Stripe (Treasury/Issuing)

Multi-currency Local Accounts

Excellent (supports 11+ major currency local clearing)

Strong (API-driven, ideal for building own card products)

API Ecosystem / Integration

High (designed for B2B / platform clients)

Medium (lightweight integration)

Medium (strong ecosystem lock-in)

Excellent (unmatched developer docs and ecosystem)

Wise

Ultimate Champion of Transparent Exchange Rates

Core Strengths

Wise uses a "local hedging" model rather than traditional SWIFT chains, reducing cross-border fees to maximum transparency

UX Insights

Its interface is extremely simplified, building strong brand trust by directly comparing bank fees through a real-time calculator

Differentiation from Airwallex

Wise primarily serves individuals and freelancers; Airwallex focuses more on enterprise clients, supporting more complex fund distribution and large-scale API integration

Revolut Business

Exceptional Fintech App Experience

Core Strengths

Revolut has extremely fast product iteration speed, with its business version covering all functions from FX and card issuance to crypto and large payments

UX Insights

Pursues ultimate interaction fluidity and consumer-product-like playfulness, skilled at integrating massive features through complex dashboards without losing logic

Differentiation from Airwallex

Revolut is more like a digital bank; Airwallex focuses more on "global payment infrastructure," with deeper advantages in acquiring and global clearing network depth

Stripe

Developer-Driven Payment Empire

Core Strengths

Stripe redefined how online payments are integrated, with its Connect and Treasury products allowing enterprises to build their own financial services

UX Insights

Design language is extremely rational and precise; its documentation design is considered the industry ceiling

Differentiation from Airwallex

Stripe's core is "acquiring (collection)"; Airwallex provides a more complete "collect, manage, pay" fund closed loop, with more flexibility in offshore accounts and complex FX scenarios

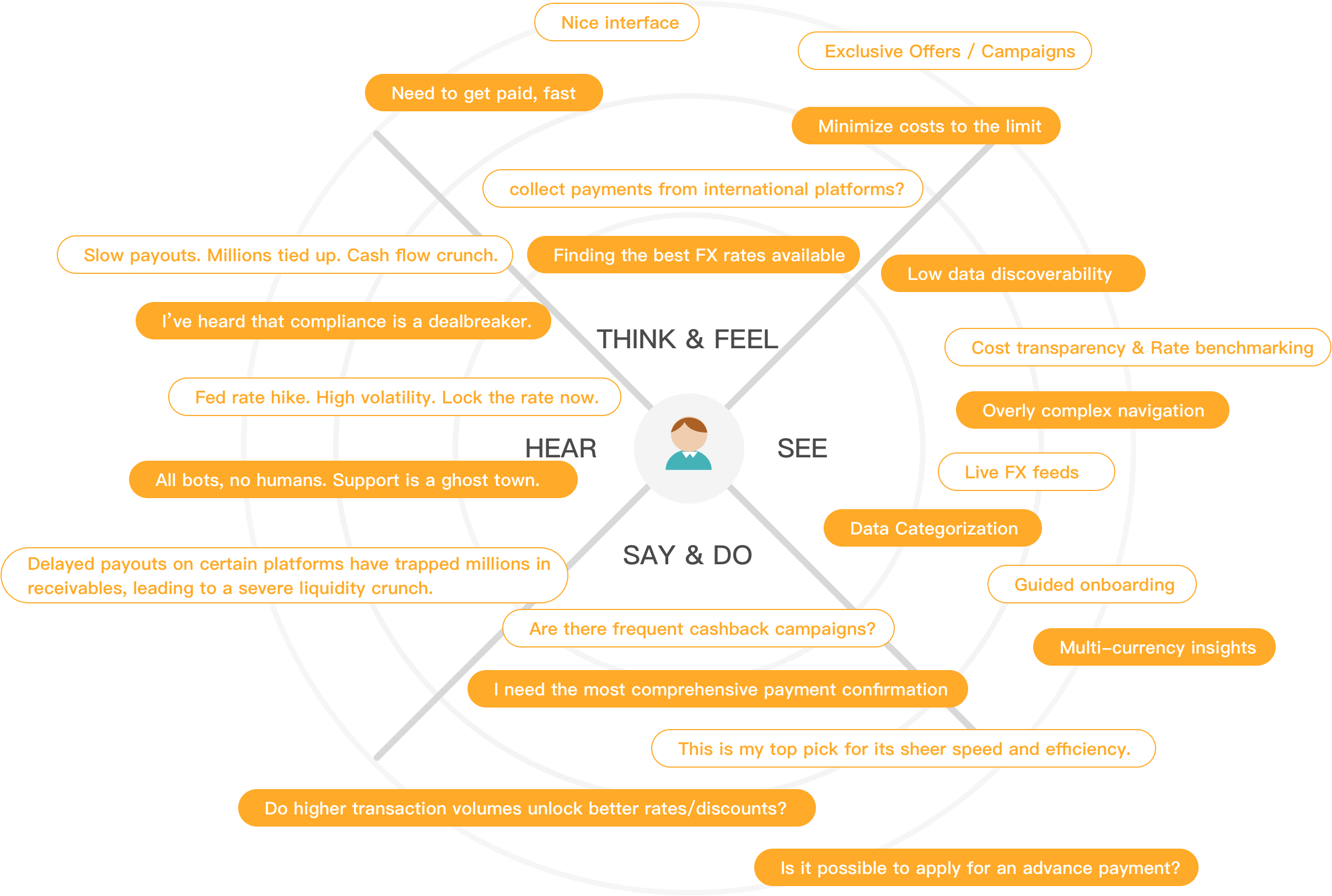

Before doing product design, what I fear most is "metaphysical" design. Therefore, studying users' actual thoughts and actions became my main work here. I divided users into core, potential and other tiers, conducting targeted in-depth interviews. I found that many times, the logic we consider "obvious" is actually very painful for users. By organizing these interview notes, I derived several design hypotheses, hoping to transform them into subsequent implemented design. This process made me understand that good design hypotheses are not invented out of thin air, but extracted from users' complaints and struggles.

Defining User Segments

In Airwallex's experience architecture design, I adopted a business-value-based user segmentation model and RFM model (analyzing user recency, frequency, and monetary value), dividing target users into four categories: core users, potential users, neutral users, and watching users, to conduct differentiated pain point analysis for each segment.

Core Users

Have multiple Airwallex products and frequently transact

Potential Users

Have multiple Airwallex products but transact infrequently

Neutral Users

Have Airwallex products but do not transact

Watching Users

Watching – do not yet have Airwallex products

Core Users

Have multiple Airwallex products and frequently transact

Potential Users

Have multiple Airwallex products but transact infrequently

Neutral Users

Have Airwallex products but do not transact

Watching Users

Watching – do not yet have Airwallex products

User Interview Guide

Basic Information

Structured interview, 5 min

– Age

– Identity

– Interests

– Company's business type

– Whether they use Airwallex products

Airwallex Client

Open interview, 15–20 min

– What type of cross-border business they are and how they started using Airwallex

– Main transaction types? Frequency? Key factors in deciding to use Airwallex?

– What are the typical steps when initiating a transaction?

– In which scenarios do they use which features of the Airwallex client?

– What did they expect from Airwallex? What did they actually get? Did it meet expectations?

– Have they used other platforms? What do competitors do well? Where does Airwallex better meet their needs?

– Were there any unpleasant experiences while using the Airwallex client? What made them unpleasant?

Other

Open interview, 5–10 min

– Any particularly memorable experience when conducting transactions in the client? What impact did it have?

– Under what circumstances did pleasant and unpleasant experiences occur?

– Can they describe a specific feature interaction design they particularly like?

User Interview Summary

To uncover the real pain points behind the product, I had deep conversations with 10 'doers' active on the cross-border front lines. They ranged in age from 20 to 40—including Gen Z overseas startup founders full of curiosity about new technology, as well as senior financial managers who have been in finance for years with an extremely stable working style.

This range gave me very interesting perspective collisions: young people care more about "can I get it done in one click," while mature managers focus more on "is every step of this money clearly controllable." It was this interweaving of diverse voices that allowed me to extract the following highly valuable interview conclusions.

Usage Habits

– First check if cross-border payment fees are low and transaction process is straightforward

– Whether transactions can arrive quickly and in full

– Whether there are promotional offers to reduce transaction costs

Behaviors

– Select products based on their transaction type for specific operations

– Need clear data and receipts to support transactions and track their status

– If unable to quickly obtain needed information, immediate human service support is needed

– Need actual cross-border services including payments, collections, and FX exchange

Preferences

– Clear and specific data display, preferring real-time data (e.g., real-time exchange rates)

– Simple and easy-to-understand product operation flows

– Clear historical data summaries with export/print service (for financial reports, etc.)

– Hope to receive feedback (e.g., transaction status, step-by-step feedback)

Design Hypotheses

Research ends not with reports, but with action. Based on in-depth interviews with 10 users of different backgrounds, I transformed those scattered pain points into a series of verifiable "design hypotheses."

01

On "Efficiency & Cognitive Load"

"If we make the complex FX calculation and fee breakdown real-time visual, users' exchange decision time will shorten, because 20–30 year old entrepreneurs prefer 'instant decisions' over post-hoc comparisons."

Design Action Add a "real-time calculator" widget in the FX interface, or directly show estimated savings compared to banksPain Point Addressed Reduce the hassle of users manually switching windows to calculate

02

On "Financial Security & Transparency"

"If we provide clearer status tracking at each node of the fund flow (acquiring-crediting-FX-distribution), user trust in the platform will increase, because 30–40 year old senior financial professionals have natural anxiety about 'unknown fund destinations.'"

Design Action Design a horizontal progress bar similar to "express logistics tracking," marking timestamps and current status at each fund nodePain Point Addressed Eliminate the "black box" fear during large transfers

03

On "Error Prevention & Recovery"

"If we introduce 'smart suggestions' and 'common payee validation' features, the chargeback rate will significantly decrease, because users are prone to spelling errors when handling complex SWIFT codes from multiple countries."

Design Action Provide auto-completion when entering bank codes and real-time validation of account number digitsPain Point Addressed Cross-border transfer errors incur extremely high fees and time costs

04

On "Multi-tasking & Dashboard Customization"

"If we allow users to customize Dashboard module priority based on their business focus, both average session time and operational efficiency will improve, because enterprises of different sizes have completely different financial priorities."

Design Action Provide a modular homepage design, allowing users to adjust the display order of key data like dragging componentsPain Point Addressed A static interface cannot meet the diverse needs from individual entrepreneurs to large enterprise finance teams

Empathy Map

Based on users' usage habits, behaviors, motivations, and preferences, we summarized the empathy map, deriving user needs and pain points.

Pain Points

– Too many data types, unclear display, unable to quickly find useful information

– No product feature guidance, unclear which area handles which business function

– High product learning curve, cannot quickly get started with operations

– Many function levels, multiple entry points, users easily get lost

– Cannot get real-time human service assistance when problems arise

– Lack of real-time feedback

Needs

– Need product usage guidance

– Improved data display to help users conduct business operations more quickly and effectively

– More promotional offers to attract users and increase transaction frequency

– More diverse and engaging interaction methods

– More direct data operations, more prominent data download function

User Personas

S

Selina

B2C Fund Distribution User

"Airwallex's fees and exchange rates are the key factors most influencing my choice of payment platform."

Goals

Hope to use Airwallex for collection services and get the latest fund and exchange rate information.

Pain Points / Needs

– High product learning curve

– Multiple feature entrances, easy to get lost

– Frequently unable to find needed information

– Hope to get exchange rates on the same day as collection

– Hope for more complete data sync and export features

Motivations / Behaviors

Collection Freq.

Remittance Freq.

Cost Sensitivity

Info Needs

SMB Cross-border Payment Operator

M

Mike

B2B Small Transaction User

"Can Airwallex more efficiently support small cross-border sellers like me to complete the full daily transaction process?"

Goals

Hope Airwallex products can meet the daily cross-border transaction needs of micro-sellers, reducing operational friction.

Pain Points / Needs

– Unaware if there are other features available

– KYC process is cumbersome and complex

– Unclear customer service response methods and channels

– Hope for more comprehensive human service support for onboarding

Motivations / Behaviors

Collection Freq.

Remittance Freq.

Cost Sensitivity

Info Needs

Cross-border Small Shop Seller

N

Nina

B2C Fund Distribution User

"Can Airwallex provide accurate real-time data to help me with financial processing and reconciliation?"

Goals

Hope to use Airwallex products combined with company business to create an efficient financial data support solution.

Pain Points / Needs

– Too many data types, difficult to find key information

– Unclear customer service response methods and channels

– Hope for improved data sync and report export features

– Download function needs to be more prominent and support multiple formats

Motivations / Behaviors

Collection Freq.

Remittance Freq.

Cost Sensitivity

Info Needs

Mid-Large Cross-border Platform Finance Handler

User Experience Journey Map

To fully examine every critical moment in the user's fund flow journey, I built this end-to-end user experience journey map. It not only records operational steps but also reveals users' emotional ups and downs when facing exchange rate fluctuations and compliance checks. By identifying these emotional low points, I locked in the core design focus: transforming uncertain financial black boxes into perceptible, transparent digital experiences.

ScenarioA cross-border e-commerce director (DTC brand) needs to exchange received USD proceeds and pay overseas suppliers

User GoalComplete a large cross-border transfer at the best rate, fastest speed, and securely

Stage

01

Fund Credit

02

FX Decision

03

Initiate Payment

04

Status Tracking

User Actions

Check multi-currency wallet balances; verify deposit details from different platforms.

Observe real-time exchange rate fluctuations; calculate FX costs; decide the right time to exchange.

Enter supplier account information; select payment route; confirm fees.

Repeatedly check if funds have arrived; export receipts to send to suppliers.

Touchpoints

Dashboard balance widget, transaction history list.

Real-time exchange rate chart, FX calculator, rate lock popup.

Payment request form, payee management.

Fund flow progress bar, email/push notifications, PDF receipts.

User Emotions

😃 Satisfaction at seeing income, but slight frustration when facing multiple transaction records.

🤨 Anxiety about exchange rate fluctuations, worried about missing the best price.

😰 Stress when filling in bank codes, extremely worried about entering wrong account numbers.

😐 Uncertainty when funds are in transit, hoping to get feedback as soon as possible.

Exchange rates not updated in time; fee calculation not transparent.

Complex entry of international bank info (SWIFT); easy errors lead to chargebacks.

Cross-border fund flow is like a "black box," unclear which node is causing delays.

Design Opportunities

Auto-reconciliation Labels: Smart identification of order sources, reducing manual operations.

Rate Alert/Transparent Breakdown: Visually show savings compared to banks, enhancing trust.

Smart Validation/Auto-complete: Real-time account format validation, introduce frequent payee feature.

Visual Logistics-style Tracking: Display fund progress to each intermediary bank like tracking a package.

Main Feature Architecture

Main Feature

Sub-feature

Navigable

Design System

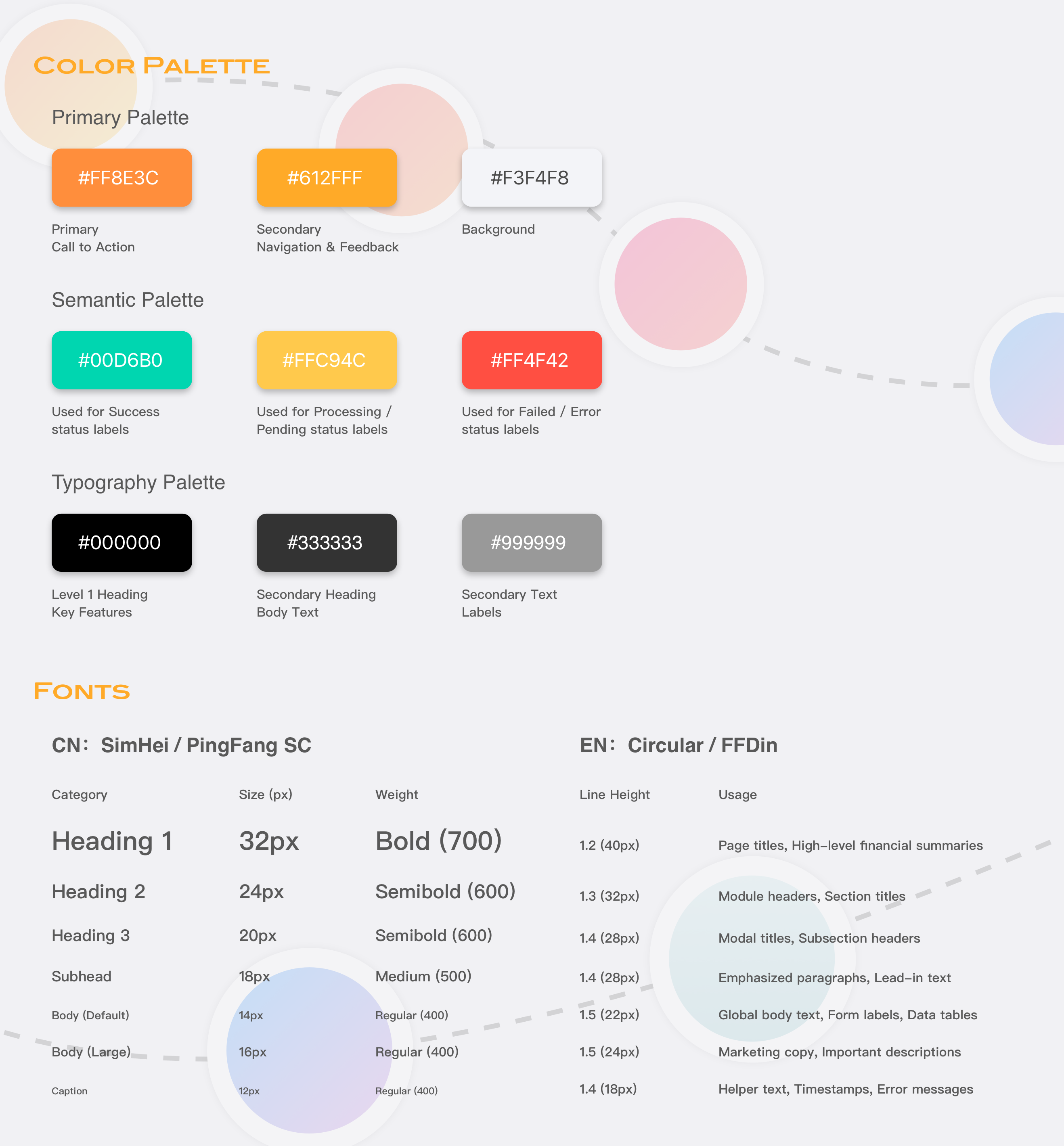

Establishing a brand design system defines the professionalism and consistency of the brand in the digital dimension. By establishing a standardized color system to strengthen semantic feedback for financial operations, paired with precise typographic hierarchy to ensure reading comfort under high-density data, laying a solid foundation for complex cross-border payment experiences.

Layout Design

Layout Structure: Clear Information Hierarchy

Keywords: Information Hierarchy, Operation Flow, Intuitive Navigation

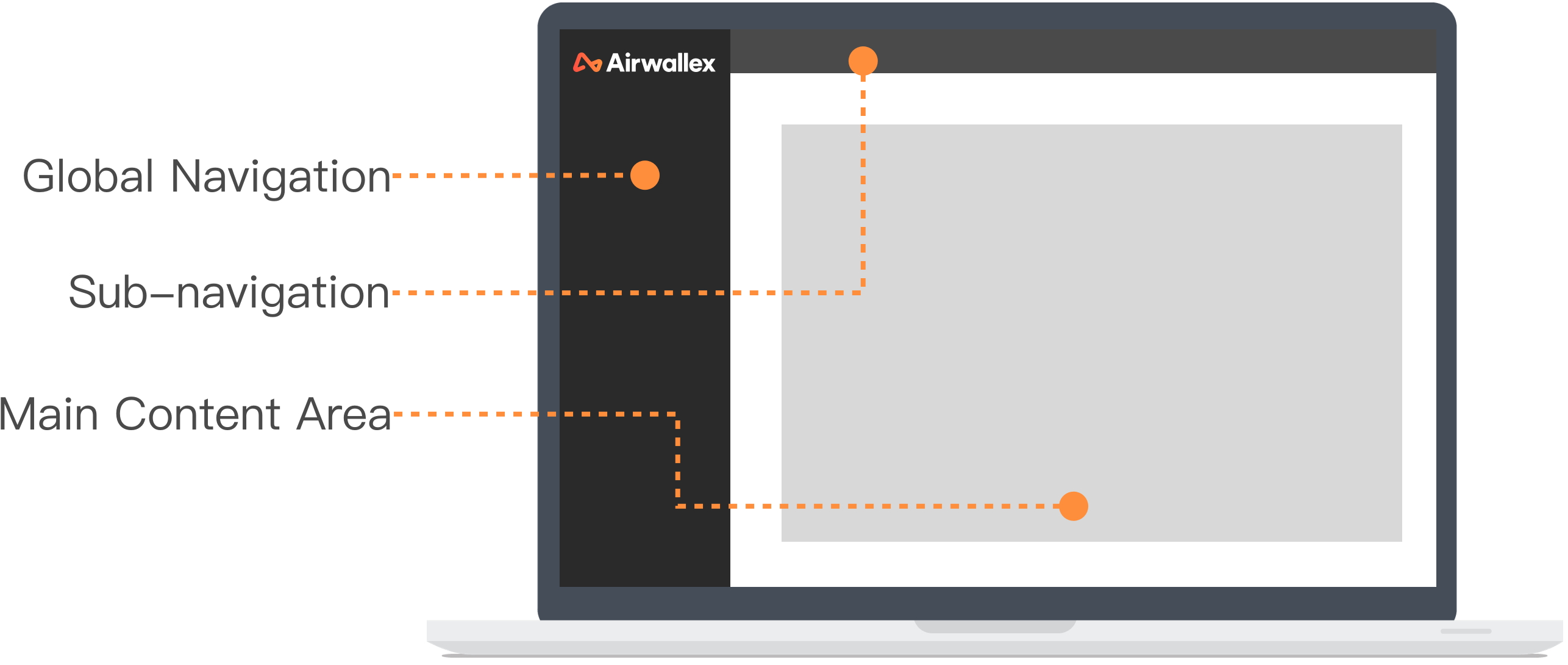

To balance high information density and ease of use in B2B products, I built this three-section layout system. Global Navigation enables seamless cross-module switching, paired with Sub-navigation for page-level frequent operations. The overall design aims to eliminate the complexity of financial business, ensuring users have clear logical direction and efficient operation flow when handling massive data.

Icon Design: Consistency & Recognizability

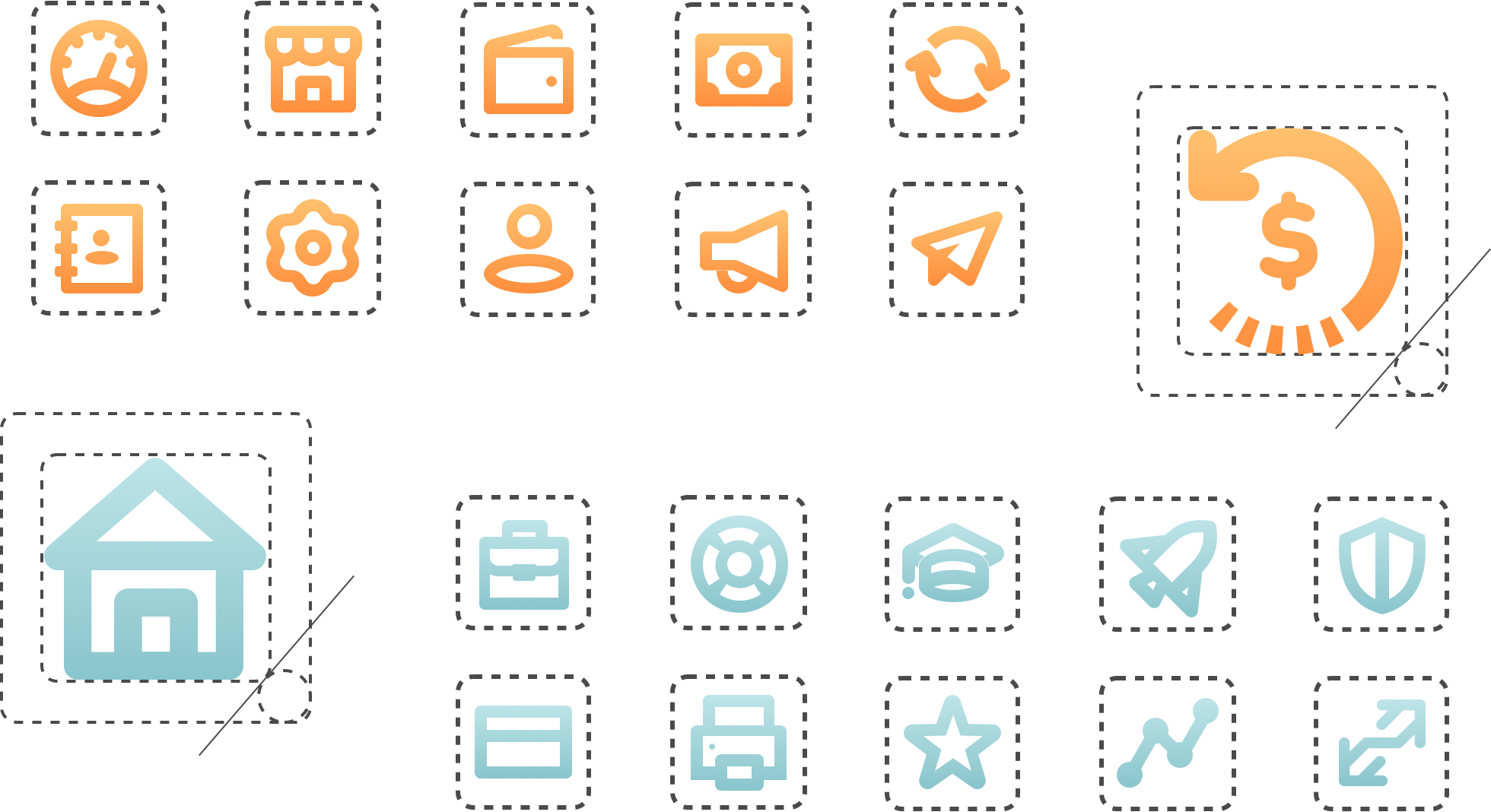

Keywords: Unified Style, Intuitive Operations, Brand Extension

The icon system uses a unified linear style; rounded corners convey approachability while maintaining the professionalism of financial products. Each icon is highly aligned with its functional semantics and operation context, ensuring users can make correct operational judgments without text prompts, reducing learning costs.